Coverages and costs. When it comes down to brass tacks, this is what matters to the insured. They want to know that their hotel insurance will cover them when they need it to and won’t cost them a small fortune.

You need to put hotel insurance coverages and costs in perspective, so you can answer the most common questions prospective clients have. With this information updated for 2022, you can reassure clients that they’re getting expertly crafted coverages designed for the hotel industry at a price point that’s competitive in the market.

What Does Hotel Insurance Need to Cover?

There is plenty of room for things to go wrong in hotels. That’s why they need broad and comprehensive insurance policies that can cover them, no matter if there’s a fire in the kitchen or a slip at the pool.

Here is a list of the coverages that many hotels need:

- General Liability: A basic GL policy helps cover claims associated with everyday business activities such as guests falling on premises, damage to guest property, restaurant operations, and accidents related to recreational activities.

- Liquor Liability: A specific liability policy designed to shield hotels from the cost of being held liable for incidents resulting from serving alcohol.

- Commercial Umbrella: A top-up policy that gives hotels additional liability coverage so they can maintain coverage limits beyond what is available on their primary GL.

- Commercial Auto: A comprehensive policy that covers commercial vehicles if they’re involved in an accident, vandalized, or stolen. It also includes auto liability coverage for costs related to property damage or injuries caused by a crash.

- Garagekeepers: A policy that covers cars that have been parked by the hotel’s valet service.

- Property: General property insurance covers the hotel business property, protecting the physical buildings and structures from covered perils.

- Cyber Liability: A policy designed to cover the costs associated with cybercrime and data breaches.

With Distinguished’s hotel primary insurance, this coverage comes conveniently bundled to give your clients more coverage and convenience at lower costs. For instance, our Hotel Primary insurance combines general liability, liquor liability, and commercial auto insurance. Property insurance available on a case-by-case basis. It also comes paired with our dedicated claims team to make you and your clients’ lives that much easier.

You can even add in high-limit hotel umbrella insurance (limits up to $170M) and cyber liability, so your clients get the comprehensive hotel insurance coverage they need. Still have doubts? Our umbrella policies backstop over 20% of hotel rooms in the country, and it’s hard to go wrong with a resume like that.

Want to learn more? Register your agency or chat with one of our insurance experts to find out more.

Why Hotels Can’t Afford to Be Underinsured

It can be easy for hotels (and any business owner, really) to decide to go for the cheapest insurance policy. But, as any insurance broker knows, that would be a colossal mistake. Hotels, in particular, need to make sure that they aren’t underinsured because so much can go wrong on their premises.

Here are just three reasons to help convince your clients that they’d rather be safe than sorry.

1. Fire and Water Damage

When you have so many people in one place, anything can happen. In worst-case scenarios, that anything can result in fires, flooding, and massive property damage. Whether it’s a misplaced cigarette leading to $250,000 in damages or a guest flooding a hotel with 400,000 liters of water, these accidents are just one mistake away from happening.

2. Accidents Around the Pool Add Up

Swimming pools and spas may be a big draw to bring in guests, but they’re also injury and lawsuit magnets. In 2022, Disney was sued for $100,000 after a woman claimed she was permanently injured when using one of their pools. If the House of Mouse can get sued in the Happiest Place on Earth, it’s probably a good idea that your client’s hotel is prepared in case it happens to them, too.

3. Human Trafficking on Hotel Premises

It’s not something that anyone wants to think about, but it’s an endemic problem in the U.S. and around the world, and it often happens in hotels. Not only are hotels seen as easy places for trafficking to occur, but they also sometimes unknowingly hire these victims to work in their hotels.

Human trafficking is obviously a heinous thing in and of itself. But from an insurance perspective, it’s also a huge potential problem that could open up the hotel to liability suits.

How Much Does Hotel Insurance Cost?

For something as wide and varied as hotel insurance, there is no one average price point you can quote your clients. However, this will not stop them from asking, and it’s always helpful to give them some kind of answer before you can get an actual quote reflecting their specific circumstances.

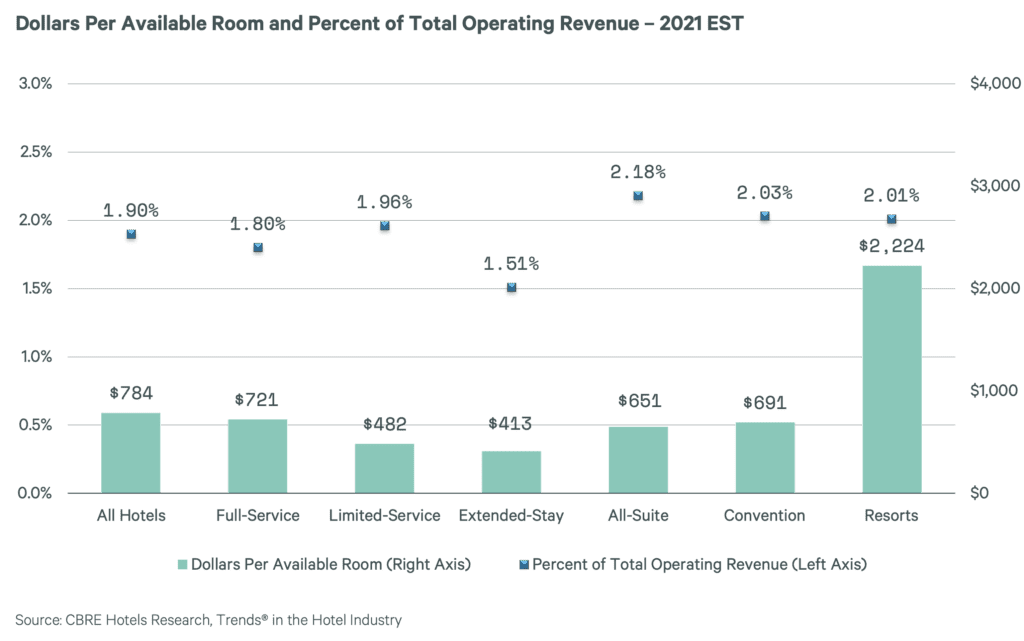

Luckily, you should be able to give them a rough estimate using some historical data and basic math. According to research done by CBRE, the average cost of hotel insurance in 2021 was about 1.9% of operating revenue. If you’d like to give a more accurate number, CBRE has also broken down the estimated cost of hotel insurance by hotel type, ranging from limited service to resorts.

Image from CBRE

Note that these costs are averages, so depending on the details of your client’s hotel, the price could be more or less. Although this chart is not 100% accurate all the time, it should be enough to give your clients the rough estimate they need before you get them a more firm quote based on their situation.

Explaining the Costs of Hotel Insurance

The above section can give your clients an idea of what their premiums might look like, but it doesn’t explain why. The following is an overview of the costs behind each coverage type and some of the factors that go into the cost of hotel insurance.

General Liability

The premium for General Liability insurance is driven by several factors, including class code, size (revenue or number of rooms), number of stories, amenities offered, and loss history. Distinguished Programs utilizes a rating system driven by the number of hotel rooms, which provides a good measure of the hotel’s exposure.

A property with a significant loss history will also see higher GL premiums. Underwriters will look at the hotel’s loss experience and its risk management practices and protocols. Better-managed risks allow underwriters to offer a more favorable premium because these hotels are actively demonstrating they are doing a good job of managing their properties.

Commercial Umbrella

As with the General Liability policy, the cost of Hotel Umbrella insurance is rated based on the number of hotel rooms. An underwriter will also look at the hotel’s loss experience, amenities for ancillary exposures, auto exposure, (including the number of scheduled vehicles on the Commercial Auto policy), and the pricing of the underlying General Liability policy.

Commercial Auto

The types of vehicles and how they’re used drive Commercial Auto insurance rates. It costs more to insure vehicles that transport guests to and from the hotel’s amenities or airport than it does to cover standard-service vehicles. Passenger transport is a large liability exposure for hotels.

Garagekeepers

Garagekeepers insurance is needed if the hotel provides valet parking. Underwriters will look at the hotel’s best practices for hiring drivers, including whether MVR background checks are conducted and the type of driver training offered when assessing risk.

Property

As with any building, construction type (building materials such as wood frame, brick, steel, or stone and age of the building), occupancy, and protection all factor into the price of Property coverage for hotels. Safety features, such as proximity to a fire station, fire protection, and safety and security protocols, are also considered when determining premiums. Amenities need to be considered as well. Restaurants are a big fire exposure for hotels. Therefore, it’s important to understand the operation’s safety practices when it comes to cooking appliances, equipment maintenance, and grease handling.

Cyber Liability

The price of Cyber insurance premiums is largely determined by the size of the hotel property. The larger the hotel, the greater its exposure and the higher the premium. More employees and guests increase the potential for breaches and other cyber vulnerabilities. This includes access to point-of-sale (POS) systems, public Wi-Fi networks, mobile-enabled key cards, and third-party data-sharing networks like online travel agents (OTAs).

Learn More About Distinguished’s Hotel Insurance

Hotels are big business for insurance companies and require a lot of expertise and knowledge to get right. If you have questions about the particulars of Distinguished’s hotel insurance offerings, please reach out to our team so we can clarify how we can help you get your clients the best possible insurance program for their hotel or resort.

If you’re interested in taking the next steps with Distinguished, you can register your agency here or explore our insurance packages on our hotel programs page.